“Social Security is one of the most effective poverty-prevention programs in history. According to the U.S. Census Bureau, it keeps nearly 29 million Americans from sliding into poverty each year,“ Larry Fink, BlackRock CEO in his 2026 letter to investors.

What Is Social Security?

At its core, Social Security is one of the most important financial safety nets in the United States – designed to provide a steady source of income when it is needed most. It supports millions of Americans, including those who are:

- Retired

- Spouses or dependents of eligible workers

- Living with a disability

- Survivors of a deceased worker

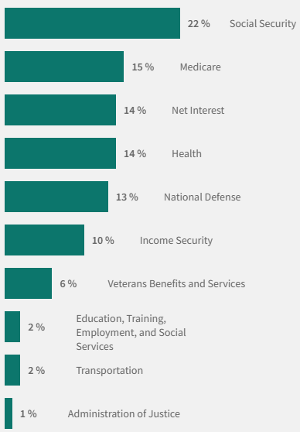

While Social Security can serve several critical roles, our primary focus is on its central purpose: delivering reliable monthly income to individuals in or approaching retirement. Before diving deeper, however, it is worth recognizing the broader scope of this program — one of the largest in the federal government, accounting for roughly one out of every five dollars spent!

U.S. Government Spending, FYTD 2026 – Top Spending by Category

Source: https://fiscaldata.treasury.gov/americas-finance-guide/federal-spending/

Social Security Disability Insurance (SSDI)

Often referred to simply as “Disability,” SSDI provides a financial lifeline for individuals whose health prevents them from working. If a serious condition limits your ability to earn an income – whether temporarily or permanently – SSDI can offer monthly support during an otherwise challenging time.

You may qualify if your disability is expected to last at least one year, result in death, or if you are legally blind. In most cases, eligibility also depends on your work history – typically having worked at least five of the last ten years – though younger individuals may qualify with fewer years of work.

Survivor benefits

Social Security also extends protection to families after the loss of a loved one. Survivor benefits provide ongoing monthly income to eligible family members of individuals who paid into the system during their working years.

You may be eligible for survivor benefits if you:

- Are age 60 or older (or age 50–59 if you have a disability),

- Were married for at least nine months prior to your spouse’s passing, and

- Have not remarried before age 60 (or age 50 if disabled).

Children of a deceased worker may also qualify. Benefits are generally available to those who are unmarried and under age 18, up to age 19 if attending school full-time (K–12), or at any age if they developed a qualifying disability at age 21 or younger.

When Can I Begin Receiving Social Security Retirement Benefits?

You can claim retirement benefits as early as age 62, but your benefit will be permanently reduced.

Key ages:

- 62 is the earliest you are eligible.

- Full Retirement Age (FRA) is between 66 and 67 and depends on the year you were born. If you were born in 1960 or later, FRA is 67.

- 70 provides the maximum benefit (no further increases after this).

If you were born in 1960 or later, you’ll receive

- 70% of your full benefit at age 62

- 100% of your full benefit at age 67

- 124% of your full benefit at age 70

Every month you delay between birthdays adds a prorated increase to your benefit. At age 70, you’ll have maximized out at 124%.

For example, based on his earnings history, Tom is entitled to $1,000 per month at age 67. If he claims early at age 62, his benefit would be reduced to $700 per month. By waiting until age 70, his benefit rises to $1,240 per month. (Keep in mind, this does not include cost-of-living adjustments, which are required by law and will gradually increase Tom’s benefit over time.)

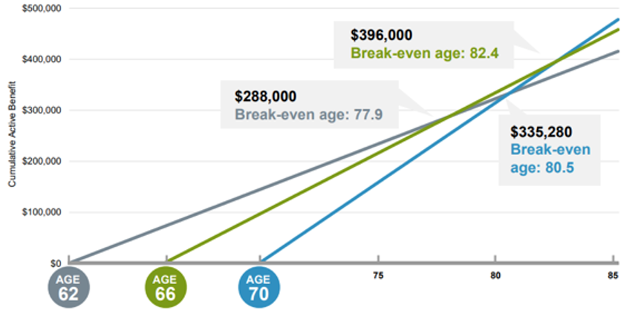

The Breakeven: Claim Now or Wait?

One of the most common questions we hear is: “If I start Social Security at age 62 and receive smaller checks for a longer period, when would I come out ahead compared to waiting?”

That’s where the concept of a “break-even age” comes in. This is the point in time when the total dollars received from delaying benefits finally surpass what you would have collected by claiming early. In other words, it’s when patience begins to pay off.

But the decision isn’t purely mathematical. Your personal health, longevity expectations, financial needs, and overall retirement strategy all play an important role. Understanding your break-even point – alongside these broader considerations – can help you make a more confident and informed decision about when to begin benefits.

In many cases, the numbers fall into a fairly consistent range:

- Claiming at 62 vs. 67 typically breaks even around age 78

- Claiming at 67 vs. 70 breaks even around age 82

- Claiming at 62 vs. 70 breaks even around age 80

Source: Fidelity. This hypothetical example assumes that the person is not working in retirement. Sample benefits do not reflect annual cost-of-living adjustments or taxes. Had taxes been taken into account, the amounts would be lower. Benefit at full retirement age in this above chart is assumed to be $2,000 per month.

When Does It Make Sense to Claim Early?

For many individuals, the decision to claim Social Security early is driven by a simple reality: you need income now. Whether due to retirement, an unexpected layoff, or limited savings, Social Security can provide a dependable stream of cash flow at a critical time.

Health considerations also play a meaningful role. If you have concerns about longevity – whether due to personal health or family history – starting benefits earlier may allow you to make the most of what you have earned.

Others choose to claim early for lifestyle reasons. They value having income sooner, while they’re still active and able to enjoy it – prioritizing flexibility and experiences today over potentially higher payments later.

That said, if you’re still working, it is important to understand that earning limits apply before reaching Full Retirement Age (FRA). Benefits may be temporarily withheld if your income exceeds certain thresholds – but importantly, those benefits are not lost forever. (We’ll cover how this works.)

When Does It Make Sense to Delay?

Delaying Social Security can be a powerful strategy – especially if you don’t need the income right away. If you have sufficient savings, ongoing employment income, or other retirement resources, waiting allows your benefit to grow meaningfully over time.

In fact, for each year you delay beyond Full Retirement Age (FRA) up to age 70, your benefit increases by roughly 8% annually. That growth can provide a significantly higher and more reliable income stream later in life. Delaying can be particularly valuable if you expect to live a longer-than-average life or are in good health. It also serves as a form of longevity insurance – helping protect against the risk of outliving your assets.

Of course, delaying isn’t the right choice for everyone. It requires balancing current income needs with future benefits—but for those who can afford to wait, the long-term payoff can be substantial.

| Claim Early (age 62-66) |

Delay Benefits (Age 67-70 |

Best Fit If You:

- Need income immediately (retirement, job loss, limited savings)

- Have health concerns or shorter life expectancy

- Prefer to enjoy income while you’re active and able

|

Best Fit If You:

- Have other income sources (savings, employment, investments)

- Are in good health and expect longevity

- Want to maximize guaranteed lifetime income

|

Key Advantages:

- Immediate, reliable cash flow

- Reduces pressure on savings

- Greater flexibility earlier in retirement

|

Key Advantages:

- ~8% annual increase in benefits after FRA

- Highest possible monthly income at age 70

- Larger survivor benefit for spouse

|

Trade-Offs:

- Permanently reduced monthly benefit

- Lower lifetime income if you live longer

- Potential benefit reductions if still working before FRA

|

Trade-Offs:

- Requires drawing from other assets now

- Delayed gratification (fewer years collecting)

- Break-even typically late 70s / early 80s

|

| Bottom Line: The right strategy depends on your income needs, health, and long-term goals. Claim early for flexibility today – or delay to maximize income and protection later. |