Q3 Market Commentary

The overall story of Q3 was a path of least resistance continuing to point to the upside, with still-solid economic data, strong earnings growth, and a resilient consumer combining with the onset of a likely Fed easing cycle and increased bullish sentiment to push major indices to repeated record highs. Continuing AI optimism, an uptick in M&A, a notable retail-investor impulse, and thoughts of supportive positioning are also helping underpin the market at quarter’s end.

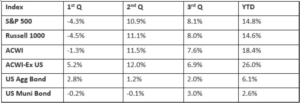

Market Performance:

Major U.S. stock indices rose 8% in the third quarter and are now up 35% since bottoming out for the year on April 8, in the wake of President Donald Trump’s sweeping tariff announcements. International stocks put in another quarter of strong performance, only slightly lagging their U.S. counterparts, and retain a more than 1000 basis point lead in performance on a year-to-date basis. Fixed income also had a strong quarter with the U.S. aggregate index up over 6% year-to-date and municipals seeing a strong recovery in the later part of the quarter bringing the return for municipals into positive territory after facing headwinds earlier in the year.

The drivers of the third quarter can be boiled down to two key drivers. First, Corporate earnings for Q2 came in well ahead of expectations and are expected to remain strong into Q3. Aggressive spending on AI remained a key element of the market narrative, with optimism for higher future investment the prevailing sentiment. AI enablers, including chipmakers, software names, and tech infrastructure firms fared very well, along with power companies leveraged to the AI theme. Complementing AI spending, consumer spending has remained firm and purchasing plans remain intact even in the face of cautious consumer sentiment. That said, while consumer resilience has been a key bullish theme, there has been rising recognition that lower-income Americans have been under great stress.

The second key driver for the markets over the course of the quarter was the shift in Fed rate forecasts. After a year of holding steady, the Fed cut interest rates at its September meeting. That brings the target federal funds rate to a range of 4.00%-4.25% with another two cuts expected during 2025 and two more in 2026. The rate cut came amid what Fed Chair Jerome Powell described as a challenging situation for central bankers. Inflation remains above target, in part due to the ongoing impact of tariffs, while the job market has cooled significantly. Investors appeared to look beyond a host of risk factors that could pull markets lower in the months ahead, including rising valuations, elevated inflation, a weakening labor market, and ongoing uncertainty surrounding US fiscal deficit and US trade policy. However, these concerns are bubbling under the surface as investors seek out diversification and perceived safe haven assets with gold powering to a record high of more than $3,800 per ounce jumping 17% in the third quarter, and the dollar remaining down 10% versus other currencies on a year-to-date basis.

Outlook

The outlook for U.S. equities remains constructive echoing the performance drivers in the latest quarter, namely expectations for solid earnings growth and lower interest rates. Earnings growth is expected to remain in the high single digit to low double-digit range over the next year, while the Fed funds rate is expected to come down closer to 3% over that period. Several structural and cyclical factors support the outlook for earnings growth: productivity and investment, looser monetary policy, easing trade uncertainty, and cost discipline at corporations. Inflation is also expected to moderate later in 2026, after peaking over the next few quarters with the roll through of the impact from tariffs. Overall, the mantra of “don’t fight the Fed” during a rate easing environment with rising earnings seems the path of least resistance for expectations of further market

gains.

However, the potential for a positive trend for the markets does not mean there will not be volatility triggered by any negative developments and intensified by the high level of valuations. Following the strong rebound from the market lows this year in mid-April, expectations for future growth have been reset higher and the probability of a recession in the next year has plummeted. Risks to the U.S. economy from weaker job growth, impact from tariffs, and lower immigration could see a slow down in economic growth in the near term, although potentially offset in 2026 by greater stimulus from legislation (OBBBA) supporting capital investment and lower interest rates.

Navigating the investment environment suggests steering a course to remain fully invested but being valuation-aware and appropriately allocated. Exposure to major investment themes such as AI infrastructure, energy transition, and industrial investment that have underpinned earnings growth particularly in mega cap U.S. equities should remain a core allocation within investment portfolios, but with valuations elevated relative to the rest of the market, long term investors should seek to be diversified. Within equities, exposure to the broader U.S. market in profitable, growing companies trading at lower valuation multiples should be a part of portfolio allocation. Another exposure should be international equities which despite outperforming U.S. equities by a wide margin in 2025 still trade at a historical discount relative to their U.S. counterparts. While the trajectory for diversified public equities is constructive, trade, policy, and geopolitical risks remain. Allocations outside of core public equities such as core bonds, privates (equity, credit, infrastructure and real estate), and strategies designed to buffer against volatility such as hedging strategies and structured products may also meaningfully improve portfolio outcomes and help investors reach

their strategic goals.

Summary

The third quarter saw strong performance across asset classes with outsized returns continuing to be realized in a narrow cohort of US mega cap technology names seen benefiting from AI, in particular. While the fundamental back drop for markets is constructive, elevated expectations seen in historically high valuations raises the risk of volatility and the potential for a lower level of returns looking forward. With the outlook still uncertain, investors should consider rebalancing their portfolios and ensure that they are properly diversified to weather any storms that may

arise.